The recently released Fifth National Climate Assessment highlights that while U.S. greenhouse gas emissions have fallen since hitting a peak in 2007, significantly deeper cuts are required to prevent catastrophic global climate change. It also notes that we are already seeing an increasing frequency and severity of hazard events due to climate change, and that increased climate adaptation efforts are needed to protect public health and life safety and to prevent property damage and economic disruption. The world suffered $313 billion in losses due to hazard events in 2022, with 75 percent of these occurring in the United States. The U.S. set a record for natural hazard events in 2023, with 25 separate events with losses of one billion dollars or more, breaking the previous record of 22 set in 2020 and far exceeding annual averages from previous decades. These impacts are rippling through the insurance industry with insurance companies pulling out of risky markets and defaulting at record rates. State insurance agencies are battling insolvency and property owners in certain areas are seeing eye-popping rate increases.

These direct and indirect climate change impacts are creating risks for commercial real estate investors, building owners, and even lenders, with increasing insurance costs, and potentially significant capital costs for damage repair, extended business disruption, or complete loss of property value after hazard events. With insurance companies pulling back, and investors seeking information on the climate-related financial risks, new regulations are beginning to require disclosures.

The U.S. Securities and Exchange Commission (SEC) is expected to release rules in 2024 that will require public companies to disclose GHG emissions and climate-related financial risks. More immediately, the State of California adopted two related laws last fall, the Climate Corporate Data Accountability Act (SB 253)1 and the Greenhouse Gases: Climate-related Financial Risk Act (SB 261)2 that apply to “covered entities” (corporation, partnership, limited liability company, or other business entities) doing business in California. SB 253 requires businesses with more than $1 billion in annual revenues to disclose their Scope 1 and 2 GHG emissions (direct emissions from energy use) starting in 2026, and Scope 3

(indirect emissions from transportation, supply chains, etc.) in 2027. SB 261 mandates that companies with more than $500 million in revenue must biennially disclose their financial risks associated with climate change and natural hazards and what they are doing to mitigate the risks beginning on January 1, 2026. This regulation is closely aligned with the Taskforce for Climate-related Financial Disclosure (TCFD)3 and other established disclosure regulations in Europe and elsewhere. While rules for implementation of these California laws are being worked out, companies will want to start now, as it will take time to prepare the disclosures. Fines for non-compliance for SB 253 and SB 261 can be significant.

Image courtesy

RiskFootprint.png

As climate-related risk assessment is new for many companies, the following is a review of what is required. First, what is meant by climate-related financial risk? SB 261 defines it as “material risk of harm to immediate and long-term financial outcomes due to physical and transition risks, including, but not limited to, risks to corporate operations, provision of goods and services, supply chains, employee health and safety, capital and financial investments, institutional investments, financial standing of loan recipients and borrowers, shareholder value, consumer demand, and financial markets and economic health.”

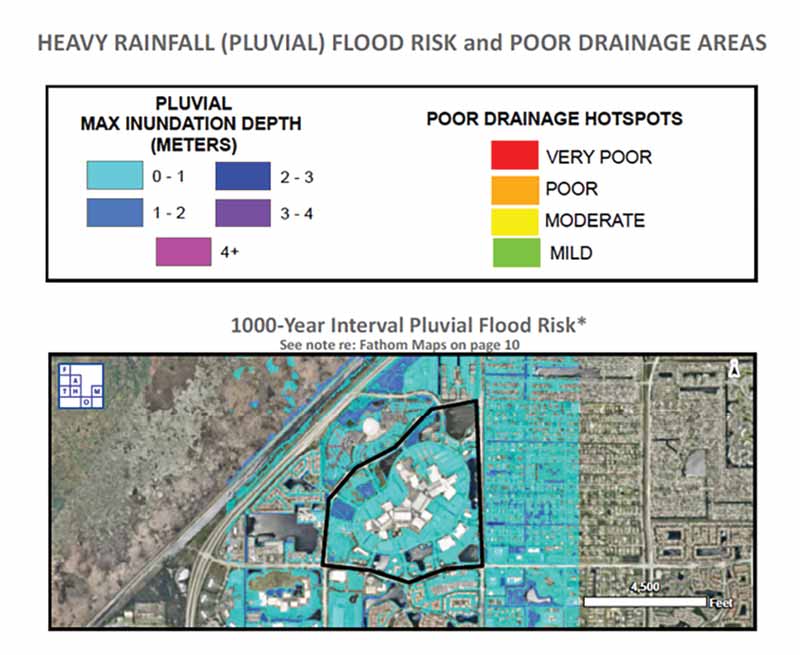

Many companies subject to SB 261 do not know which of their “core” portfolio assets have the greatest risks and, whether taken individually or together, which ones represent potential significant financial risks. Companies with multiple assets will want to start with a risk assessment across their entire portfolio. Initial portfolio risk scoring allows a company to discover which of its core assets are at high risk of significant loss of revenue or value if they were damaged by climate-related hazard events. In this way, the high-risk, core assets can be triaged for greater scrutiny. In most cases, current and future physical risks due to natural hazards and climate change are very localized, so risk and vulnerability are best assessed at the asset level. A minor difference in topography or location could significantly change the risk of flooding, storm surge, sea level rise, landslides, wildfires, or other hazards.

Once high-risk core assets are identified, a deeper assessment should be performed to quantify the sensitivity, vulnerability, and value-at-risk for each one. This may require on-site investigations by qualified professionals to assess the state of critical components and systems and their unique vulnerabilities to the identified hazards with greatest anticipated severity and probability. This might include the likelihood of electrical, mechanical, and elevator equipment being inundated by flood waters, or the soundness of the roof assembly to withstand anticipated high wind events, or other hazard- and property-specific vulnerabilities.

Based on the vulnerabilities revealed, building professionals can identify feasible risk mitigation measures with estimated costs and expected return on investments. A company can then develop a multi-year capital improvement plan for these core assets to budget and implement resilience enhancements and reduce climate-related financial risks. In some cases, the implementation of risk mitigation measures could also be used to negotiate more favorable insurance rates. In other cases, resilience measures, like on-site energy generation and storage to provide for continuity of operations or thermal enclosure improvements to increase extreme heat resilience, will also reduce utility costs and cut GHG emissions, providing additional benefits.

While there is still time to avert the worst impacts of climate change, it is already reality, and businesses and governments alike must simultaneously address both mitigation of climate impacts through GHG emission reduction and adaptation to current and future climate-related hazards though asset-level resilience investments. Assessing and addressing climate-related financial risks is now a legal requirement for many thousands of companies doing business in California and an expectation of investors, insurance companies, and regulators.

NOTES

1 www.pbs.org/newshour/nation/analysis-the-potential-global-impact-of-californias-new-corporate-climate-disclosure laws#:~:text=Under%20the%20new%20Climate%20Corporate,starting%20in%202026%20and%202027.

2 https://leginfo.legislature.ca.gov/faces/billNavClient.xhtml?bill_id=202320240SB261.

3 www.fsb-tcfd.org.