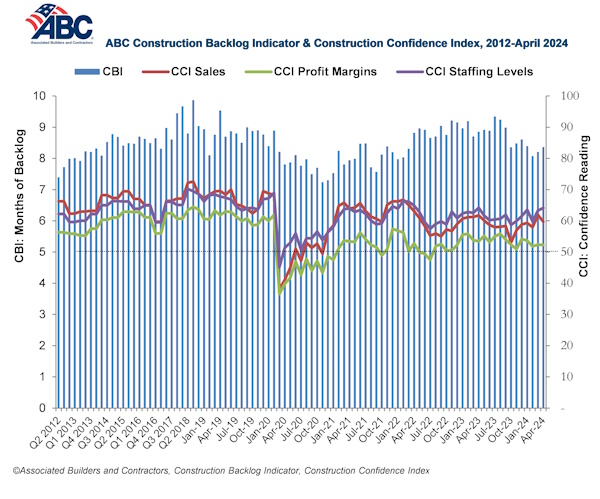

Associated Builders and Contractors (ABC) reported its Construction Backlog Indicator increased to 8.4 months in April, according to an ABC member survey conducted April 22 to May 6. The reading is down 0.5 months from April 2023, and up 0.2 months from the prior month.

Visit ABC’s website to view its Construction Backlog Indicator and Construction Confidence Index tables for April.

Backlog declined on a monthly basis for the largest and smallest contractors by revenue, and grew for those with $30-$50 million and $50-$100 million in annual revenues. On an annual basis, only contractors with $30-$50 million in annual revenues have experienced an increase in backlog.

ABC’s Construction Confidence Index readings for sales and profit margins fell slightly in April, while the reading for staffing levels improved. All three readings remain above the threshold of 50, indicating expectations for growth over the next six months.

Anirban Basu, chief economist at ABC, says, “The Federal Reserve began ratcheting up interest rates more than two years ago, but one would not know it based on construction confidence and backlog. ABC measurements reflect ongoing momentum in the nation’s nonresidential construction sector. While there are occasional hints of softness in certain segments and over certain periods, the average contractor continues to report solid backlog and a belief that sales, employment and profit margins will expand over the next six months.

“Time will tell whether this optimism is justified,” Basu says. “Coming into the year, many expected that interest rates would fall markedly in 2024. Given stubbornly elevated inflation, that will not occur. Project financing costs are poised to remain higher for longer. Project cancellations and postponements have been on the rise. Moreover, a new set of supply chain issues has emerged, driving up materials costs and prospectively weakening industry margins. Workers also are becoming more expensive, in part because the construction wage premium has shrunk over the past several years due to rapidly rising compensation levels in competing segments like logistics and retail. The implication is that construction compensation levels will need to rise for the industry to be able to staff up more fully.”