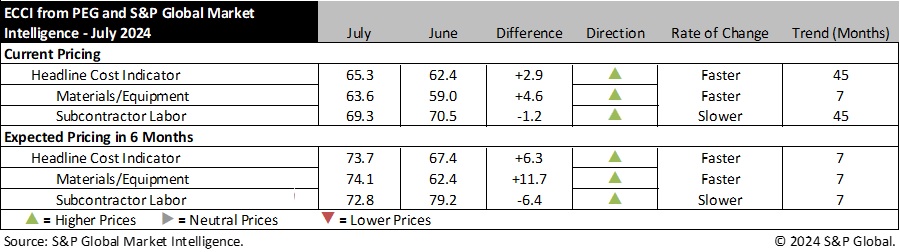

Engineering and construction costs increased in July, according to the Engineering and Construction Cost Indicator from PEG and S&P Global Market Intelligence. The headline Engineering and Construction Cost Indicator, a leading indicator measuring wage and material inflation for the engineering, procurement and construction sector increased 2.9 points to 65.3 in July.

The sub-indicator for materials and equipment costs rose 4.6 points to 63.6, while the sub-indicator for subcontractor labor costs edged down to 69.3 in July from 70.5 in June.

The materials and equipment indicator increased in July and continues to show rising prices. Seven of the 12 components increased compared to June, with the largest increases coming for carbon steel pipe, alloy steel pipe, and copper-based wire and cable. Despite increases of 14.4- and 11.7-points respectively, carbon steel pipe and alloy steel pipe remain in contractionary territory with readings of 41.7. They were joined by fabricated structural steel, which declined 0.6-point to 35.7. Copper-based wire and cable saw a 12.3-point increase resulting in a reading of 71.4 in July.

Increases for shell and tube heat exchangers, pumps and compressors, and gas and steam turbines were moderate in July, and all resulted in readings between 57.1 and 58.3. Electrical equipment and transformers each saw minor declines in July, but remain elevated with readings of 85.7. The two ocean freight categories saw a divergence in July, with routes from Asia to the U.S. falling 20.1-points to 68.8, while routes from Europe to the U.S. saw an increase to 87.5 from 81.3 in June.

Keyla Martinez, economist at S&P Global Market Intelligence, says, “Ocean freight to the U.S. East Coast has seen a recent push forward in seasonal demand in an attempt to avoid potential negative impacts as a result of ongoing union contract negotiations in the region. Combined with an era of global reduced shipping capacity, this shift in timing has driven freight rates for shipping from Europe to the U.S. higher. Rates should begin to reverse by the end of the third quarter as the earlier peak season fades.”

The sub-indicator for current subcontractor labor costs saw very little movement in July with a 1.2-point decrease compared to June. This came as a result of increases in the U.S. South region and Midwest being offset by declines in the U.S. West and both regions in Canada.

Readings for mechanical and instrumentation and electrical workers in the U.S. South each saw double-digit increases to readings of 90 in July. Subcontractor labor in the civil industry saw a 8.9-point increase to 70. Meanwhile, most employment categories in the U.S. West and Canada saw double digit decreases, and settled at neutral readings of 50 in July.